A rate hike - what's that?

It has been so long since the Federal Reserve has raise interest rates in the US that Banks and Brokerage houses are having seminars for their workers to help them understand the repercussions of a rising rate environment. If you are working with Mortgage Brokers or Financial Planners under the age of 35 - then it's very possible that in their entire professional careers, they have never been in an economic environment like this. Even for the older market professionals and traders, it's been so long it's hard to remember.

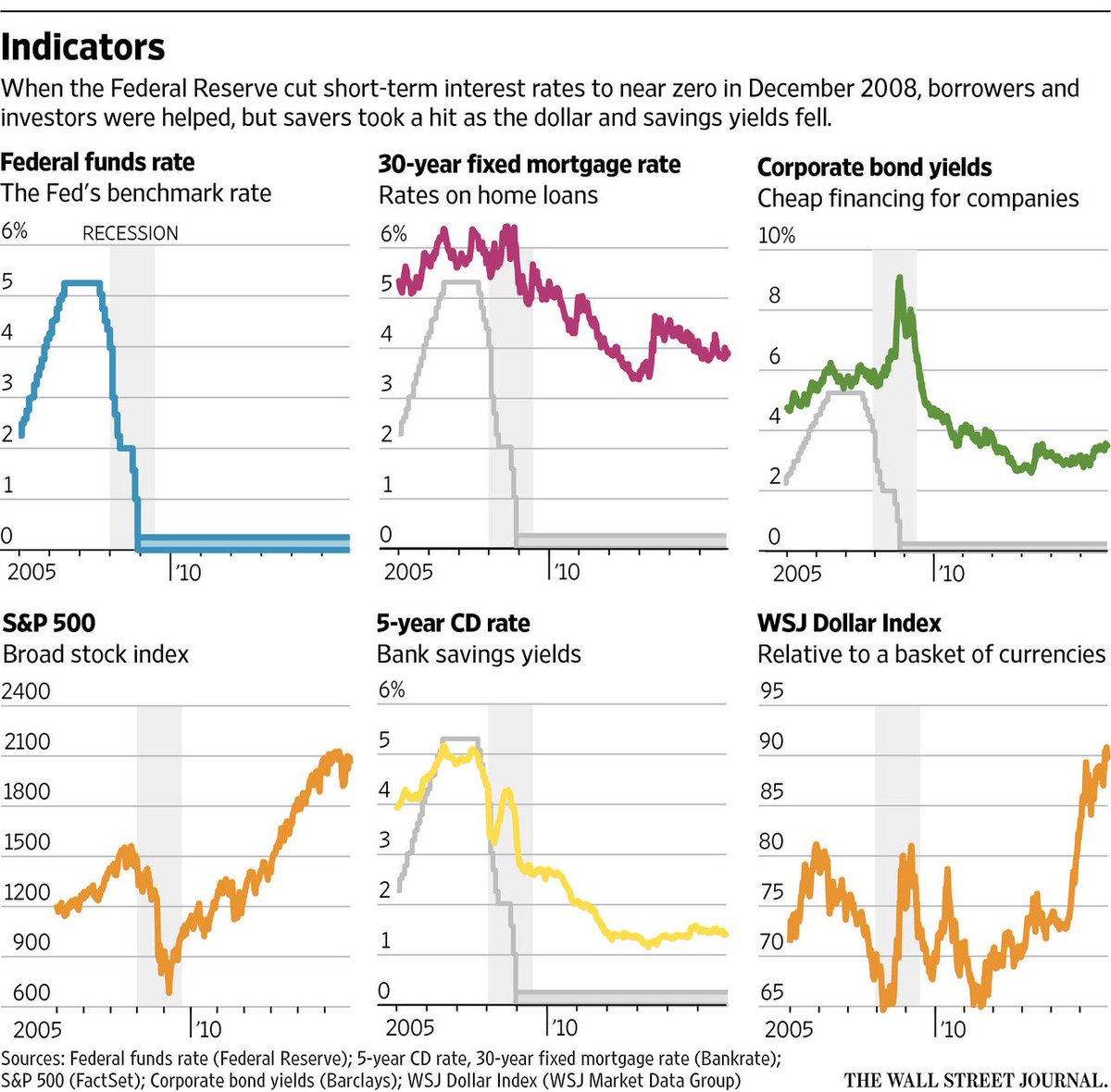

The Fed last began tightening rates back in June of 2004 mainly to cool a rapidly rising housing market but also to cool off the "irrational exuberance" in the stock market, as the S&P had gone from 800 in August of 2002 to 1,300 in April of 2006 (up 62.5%) while housing prices had doubled off their mid 90's lows. The pace of that tightening was 1% every six months, topping out at 5.25% 2 years later:

As you can see - it had a bit more than the desired effect on the housing market though housing prices continued to go up all the way into 2006 before completely collapsing almost all the way back to where they were 10 years earlier - a real "lost decade" for home buyers. Only then did the ripple effects spill out to the stock market and it was the mortgage lenders themselves and the Financial Institutions that traded their collateralized debt that ultimately took the economy down.

It would seem the Fed has gotten smarter and is not going to even let a runaway housing market get started this time - and that's a smart choice by them as we sure can't afford another round of bailouts and the low rates have let most homeowners survive the downturn, albeit without the gains they hoped they would make from their housing investments.

Since our September, 2011 lows on the S&P at 1,100, the S&P has climber 950 points, which is 86.3% and Janet Yellen has already said that's a bubble she is wary of. It's very doubtful that the Fed will tighten as aggressively as they did in the 2004-6 cycle and a big thing we'll be watching today is what kind of signals they do give as to their future intentions. As I mentioned on Monday, Hilsenrath (the Fed Whisperer) has already prepared the faithful for a gentle, gradual tightening process but we've been at almost zero for so long - almost any increase will seem huge to spoiled borrowers.

As rates rise, the Trillions of Dollars of Corporate Bonds that were purchased as low rates will begin to lose their value on the secondary market. Verizon (VZ) for example, sold $49Bn worth of 5% debt (all at once) in 2013 and has since refinanced it at even lower rates. That's great for VZ but it won't be so good for people holding 5% and lower corporate bonds as "safer" Treasuries begin to rise to match the yields.

Anyone with a portfolio knows a loss is a loss when you are staring at it and, with 10-year notes at 2.15%, heading to just 3% will knock the value of $2Tn worth of corporate bonds down by 10-20% on the resale market. We're talking $200-400Bn in paper losses on somebody's balance sheet! Although, it's no sure thing as yes, 10-year notes jumped 33% when Greenspan first began tightening in 2004 but they went back down several times as no one really believed the high rates would last 10 years (and they were right!). At the time, Greenspan called it a "conundrum."

Another thing that happens in a rising rate environment is home refinances dry up very quickly. Obviously, no one wants to refinance their loans for higher rates and that will prevent people from taking money out of their homes leaving less money to spend in the economy. Of course home sales will also come under pressure as mortgage rates rise.

This could be the end of 0% financing on cars, furniture, etc. as well as teaser rates on Credit Card Debt and $1.3Tn of student loans are geared to the Fed Funds Rate - making them all the more harder to pay off with those minimum wage paychecks. With Corporations cut off from easy cash, we may finally see a decline in stock buybacks and M&A activity and that, of course, will not be a positive for the markets.

According to the WSJ, $541Bn has already been withdrawn from risky Emerging Markets in 2015 and the Fed hike may push that number much higher. Corporate Debt Ratios in emerging markets have jumped by 30% of their GDP in the past 5 years - clearly an unsustainable pace and potentially a disaster as the rollovers become more and more expensive. That's why, so far, the Fed is the loan wolf among Central Bankers in moving towards raising rates. Others are still looking to go lower, some EU Banks are already negative.

Back in September, the IMF's Christine Lagarde begged the Fed to wait until 2016 to raise rates "because of the implications for developing nations." Lagarde said that she is concerned that many emerging markets may have expended their capacity to buffer against shocks in the wake of the financial crisis. In a much-ignored IMF report back in October, it was esimated that Emerging Markets have over-borrowed by roughly $3Tn:

The IMF estimates developing nations—led by China—may have over-borrowed by roughly $3 trillion, and is warning that those countries could face a wave of corporate defaults. The fund estimates around 25% of China’s corporate debt is at risk, especially in the real estate and construction sectors, and including many state-owned firms.

That “will unavoidably entail some corporate defaults, the exit of a number of nonviable firms, and write-offs on nonperforming loans,” they said.

We are, of course, already seeing those defaults begin to hit - this is why we went short on China at the dead top on April 9th(FXI was $51.24, now $35.64 - down 30%) and I was banging the table to get out of China all that month. In fact, we were the only people who even noticed that Chinese bond defaults were becoming a problem that early on:

Thursday Thrust (4/9) – Peak China Achieved

Wednesday’s Worrying Time Bomb (4/15) – Global Debt Past $200Tn

Manchurian Monday (4/20) – $194,000,000,000 More Stimulus from China!

Bad News is Still Good News in China as Poor PMI Boosts Market (4/23)

Friday Failure (4/24) – Kaisa Bond Default Underlines China Housing Crash

Monday Madness (5/2) – Weak Chinese Data Spurs Stimulus Hopes

I know, I sounded like a broken record, didn't I? Well, if I got just SOME people to get out of China before it all collapsed, then it was worth it. In May (and that last post was 5/2), we finally had a little scare in China but then it rallied but then it completely and utterly collapsed, never to recover (so far) yet the US markets have been chugging along (and we are "Cashy and Cautious" on those now).

Another factor to consider is currency valuations. If the Fed hikes while other remain at ease, then the Dollar may get stronger against other currencies (it's already at 10-year highs). That puts more downward pressure on commodity prices (priced in Dollars), which many Emerging Markets depend on to survive. While it's good for their exports, it also devalues any bonds they sell in their local currency as the relative value of bonds priced in Euros, Yen, Yuan, Aussie Dollars, Loonies, etc falls compared to bonds priced in greenbacks.

Remember, China did everything they could to prevent a collapse and it still happened. How do you think other countries will do if faced with the same pressure as defaults begin to rise?

Let's be very careful out there!

-- This feed and its contents are the property of The Huffington Post, and use is subject to our terms. It may be used for personal consumption, but may not be distributed on a website.